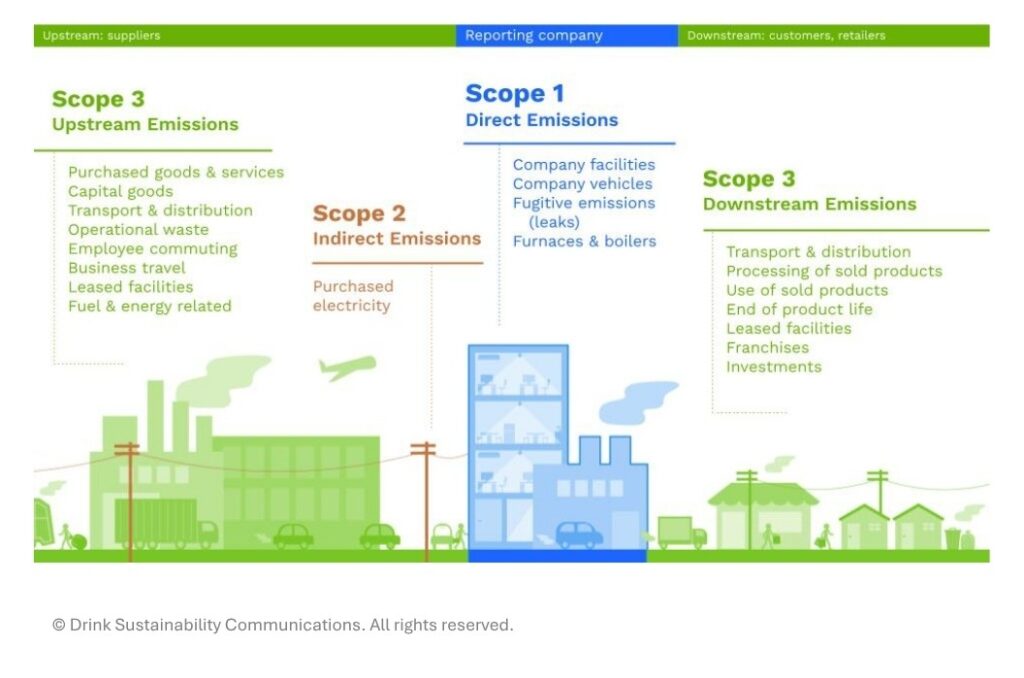

Greenhouse gas (GHG) emissions come from various origins. In GHG accounting, we divide them into three scopes to help better understand these emissions, their origins, and the point in the business operation where companies produce them. Among the three Scopes of GHG emissions, Scope 3 often appears as the most complex and data-intensive. Unlike Scope 1 and 2, which rely on internal records like fuel logs or electricity bills, Scope 3 emissions occur across a company’s value chain, making them harder to track but just as critical. (Learn more about Scope 1 and 2 emissions in the Hidden Potential of Scope 2 Emissions)

Scope 3 emissions divide into upstream and downstream emissions. Upstream emissions usually involve suppliers, whereas downstream emissions usually involve customers and retailers. For example, upstream emissions include Category – 1 Purchased Goods and Services, Category 6 – Business Travel, and Category 7 – Employee Commuting. Downstream emissions cover areas like Category 10 – Processing of Sold Products, Category 11 – Use of Sold Products, and Category 12 – End of Product Life. In total, you can find 15 categories under Scope 3 emissions that divide into their upstream and downstream classifications here along with examples of Scope 1 and 2 emissions.

To break things down further, we present the 15 categories under Scope 3 emissions in two tables: one for upstream emissions (Categories 1 to 8) and another for downstream emissions (Categories 9 to 15). We defined each category using the GHG Protocol Technical Guidance for Calculating Scope 3 Emissions and included specific data examples for your reference.

| UPSTREAM EMISSIONS | ||

| Scope 3 Category | Definition | Examples of Data Covered |

| 1 – Purchased Goods and Services | Emissions from the production of purchased goods and services | Quantity and type of raw materials Office supplies Packaging materials |

| 2 – Capital Goods | Emissions from the production of purchased capital goods | Construction materials for buildings Machinery and equipment purchased Company vehicles |

| 3 – Fuel and Energy Related | Emissions from extraction, production and transportation of fuels and energy purchased not included in scope 2 | Upstream emissions from purchased electricity Generation of purchased energy Specifically fuels purchased to generate electricity, steam, heat and cooling |

| 4 – Transport and Distribution | Emissions from the transportation and distribution of inbound goods | Third-party logistics emissionsAir freight, trucking, etc. Distance and mode of transport of purchased goods |

| 5 – Operational Waste | Emissions from disposal and treatment of waste generated during operations | Office wasteHazardous waste treatmentRecycling and landfill emissions |

| 6 – Business Travel | Emissions from employee travel for business purposes | Domestic or international flights Hotel stays Rented vehicles |

| 7 – Employee Commuting | Emissions from employees traveling to and from work | Daily commute distances and modes of travel |

| 8 – Leased Facilities | Emissions from leased assets operated by the company that were not included in Scope 1 or 2 | Emissions from leased warehouses or office spaces |

| DOWNSTREAM EMISSIONS | ||

| Scope 3 Category | Definition | Examples of Data Covered |

| 9 – Transport and Distribution | Emissions from the transportation and distribution of sold products leaving the company | Shipping to customers Third-party delivery services |

| 10 – Processing of Sold Products | Emissions from the processing intermediate products sold | Energy used by customers to process goods (e.g., manufacturers) |

| 11 – Use of Old Products | Emissions from the use of products sold | Fuel burned by vehicles soldEmissions of sold products over their expected lifetime |

| 12 – End of Product Life | Emissions from the disposal and treatment of products sold | Recycling and landfill emissionsPackaging disposal |

| 13 – Leased Facilities | Emissions from assets leased to other entities | Energy used in leased propertiesLeased equipment emissions |

| 14 – Franchises | Emissions from operations of franchises not owned by the reporting company | Energy use in franchise locationsWaste and transportation emissions |

| 15 – Investments | Emissions from companies in which reporting company has shares | Equity and debt investments Project financeManaged investments and client services Emissions data from investee companies or projects |

Scope 3 may seem overwhelming at first, but it offers the most comprehensive view of a company’s true carbon footprint. Once businesses overcome the initial learning curve, they can use Scope 3 data to identify inefficiencies, reduce waste, and make more cost-effective decisions across their value chain. Scope 3 emissions add another piece to the picture of normal operations in a company because they are not limited to what goes on in the office, factory, or plant.

Scope 3 emissions may be the most challenging to measure, but they also offer the greatest opportunity for impact. By looking beyond the office or factory and into the full value chain, companies uncover hidden inefficiencies, reduce waste, and make more sustainable choices. Embracing Scope 3 accounting isn’t just about compliance; it’s about gaining a deeper understanding of operations and making smarter, more responsible, and intentional decisions.